In recent years, housing prices in major cities have surged, pushing the dream of homeownership further out of reach for many young people. Rising inflation, unstable income, and the burden of daily expenses during early career stages have created significant challenges for those striving to own a home.

In this context, home loans with competitive interest rates and flexible tenors offers a practical path to achieving the dream of owning a first home. Choosing the right financial partner with tailored loan packages, transparent interest rates, and a clear repayment plan can make homeownership accessible and stress-free within your financial means.

Young generation’s journey to homeownership amid rising housing prices

Young people are becoming more proactive in financial planning and seeking homeownership opportunities, despite continuously rising prices

Statistics from Batdongsan.com.vn show a clear shift in demand for 2025: 62% of real housing demand comes from the under-35 age group. Despite this high demand, this group faces numerous barriers early in their careers. Apartment prices in "megacities" like Hanoi and Ho Chi Minh City have reached 89 - 100 million VND/m² in 2025, meaning a typical apartment requires an investment of 5 - 6 billion VND (1). This massive gap between housing prices and average income far exceeds the affordability of those under 35.

Even saving 20 - 30% of one's monthly income for a home down payment takes a significant toll on total earnings. Additionally, home loan rates and unpredictable financial market fluctuations may cause hesitation when deciding whether to take out a home loan or not.

4 "financial traps" hindering young people from mortgage financing

For those who are building their financial foundation, it is crucial to avoid these 4 "financial traps" when opting for an installment-based home loan:

1. Misunderstanding the nature of the loan

Many young individuals aspire to own a home early to secure stability, yet often lack a clear 5-10-year financial plan. The "FOMO" (Fear Of Missing Out) mentality may create financial pressure for both themselves and their families.

Understanding the nature of home financing solutions and establishing a safe financial rule of thumb is to ensure monthly debt-to-income ratios do not exceed 35 - 40% of net income. Home loan should only be considered when at least 30% of the property value has been reserved in advance, helping reduce debt pressure and minimizes the total interest paid over the home loan cycle. Instead of opting for 25-30-year tenors, consider a 15-20-year duration to optimize the total interest costs.

2. Failing to prepare for interest rate fluctuations

Home loan rates usually consist of 2 phases: an initial teaser/ promotional rate and a floating rate based on market fluctuations. Without forecasting rate trends, you shall risk a sudden spike in costs.

To mitigate risks, analyze the post-incentive rate formula and evaluate your family's repayment capacity over the next 3 to 5 years:

- Is there any option for interest rate after promotion?

- Margin: Is it fixed or variable?

- Adjustment cycle: How often does the bank reprice the interest rate?

3. Lack of understanding about home loan terms and conditions

Beyond interest rates, many customers are not fully aware of ancillary costs, causing their financial plans to deviate from expectations.

4. Neglecting a financial safety net

Maintaining an emergency fund equivalent to at least 6 - 12 months of loan repayments, representing 20 - 30% of your monthly income is necessary. This serves as a buffer against potential risks such as reduced income during economic downturns, job loss due to market volatility, or rising living costs.

If your primary income is not yet stable, consider reducing your loan-to-value ratio, choosing a home within your means, and leveraging side hustles or passive income streams.

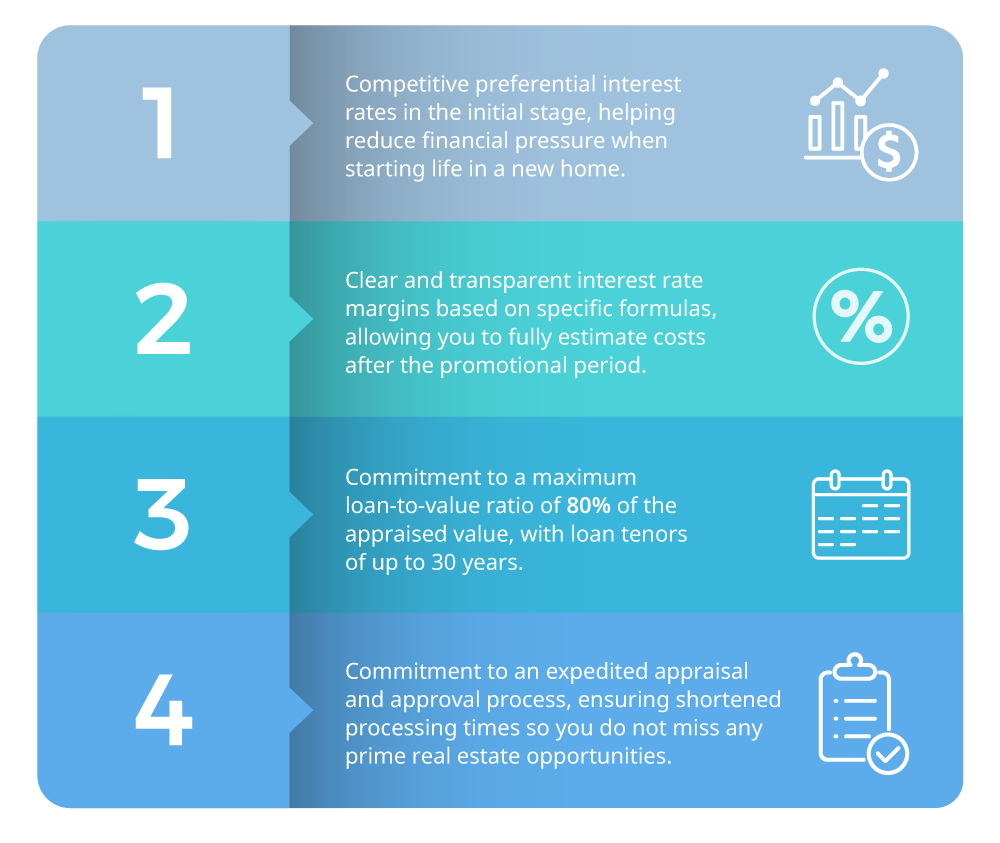

Tips for safe home financing with competitive rates from UOB Vietnam

In the journey of supporting customers on their homeownership dreams, UOB Vietnam recognizes that a home loan is more of a financial plan with a long-term vision, not only interest rates.

1. Assessing financial capacity before borrowing

We always recommend that customers:

- Only borrow when already having at least 30% of the property value as equity.

- Maintain a safe debt-to-income ratio not exceeding 60% of monthly income.

- Maintain a contingency fund equivalent to 6 - 12 months of loan repayments.

2. Choosing flexible loan packages with stable and transparent interest rates

Understanding the "settle down and thrive" needs, UOB Vietnam offers flexible home loans and future interest rate options tailored to various customer segments:

Above all, our advisory team is always alongside customers to clarify every term, forecast interest rate risks, and suggest optimal solutions.

3. Selecting an appropriate loan tenor

The loan tenor directly determines the monthly installment amount and the total interest expense.

- Short-term loans help save on interest but require a strong cash flow.

- Long-term loans reduce the monthly burden but come with higher total interest costs.

UOB Vietnam provides home loan solutions with tenors of up to 30 years for home purchases and 25 years for mortgages. The maximum tenor for each case depends on the customer's age (the maximum age at the end of the loan contract is 65, depending on the customer segment).

4. Proactively managing cash flow after borrowing

Signing the loan contract is only the beginning. To make the home loan more manageable, you need to have a clear monthly budget and monitor cash flow, income - expenses, and periodic debt repayments. Simultaneously, you may need to develop additional passive income streams to support faster loan redemption.

UOB HomeStar Loan: Partnering with you on the journey to homeownership

Optimize borrowing costs, reduce financial pressure, and get closer to your dream home with the HomeStar loan package

With the UOB HomeStar loan package, you can confidently move closer to your dream home with competitive interest rates starting from 3.1% p.a. Notably, the floating rate equals the mortgage rate minus 3.6%, helping you save up to 50% on interest payments. You can perform a trial calculation of the loan and estimated interest through our interest calculator, based on the total loan amount and tenor you provide.

We also provide a list of real estate projects from reputable partners affiliated with the bank. This list is updated periodically, offering you more reliable options for your dream home. During the contract signing process, with a rigorous and transparent credit assessment system and a dedicated advisory team, you can be fully assured that your loan application will always be processed most quickly and accurately.

Once you have a clear financial plan and choose the right partner bank, the home-buying journey becomes easier. If you are preparing for this important decision, we are always ready to support you.

Conclusion

Buying a home is one of the most significant financial decisions in a person's life, directly impacting personal and family finances for many years. Building a clear home-buying plan helps you own an asset while ensuring long-term stability. UOB Vietnam is committed to accompanying you on the journey of building a sustainable home with optimal, transparent, and flexible home loan solutions tailored to your needs.

Contact us for a consultation and schedule an appointment for home loan advice with UOB Vietnam.

This article shall not be copied, distributed or used by any individual or organization for whatever purpose. This article is given for reference only, non-binding and is strictly for information only. The information contained in this article is based on certain assumptions, information and conditions available as at the date of the article and may be subject to change at any time without notice. You should consult your own professional advisers about the issues discussed in this article. Nothing in this article constitutes accounting, legal, regulatory, tax or other advice. This article is not intended as an offer, recommendation, solicitation, or advice to purchase or sell any investment product, securities or instruments.

United Overseas Bank (Vietnam) Limited and its employees have made reasonable efforts to ensure the accuracy and objectivity of the information contained in this article, however, no representation or warranty, whether express or implied, is given as to its accuracy, completeness and objectivity and accept no responsibility or liability for any error, inaccuracy, omission or any consequence or any loss or damage howsoever suffered by any person arising from any reliance on the views expressed and the information in this article.