Driven by a surge in mega rounds with 10 out of 13 deals attracting at least US$100 million in funding for late-stage FinTech firms

Ho Chi Minh City, 11 November 2021 – Financial technology (FinTech) funding in ASEAN rebounded strongly in 2021, up more than three times in the first nine months of 2021 compared with full year 2020 to an historic high of US$3.5 billion. According to the FinTech in ASEAN 2021 report by UOB, PwC Singapore and the Singapore FinTech Association (SFA), the rebound in FinTech funding was driven by 167 deals including 13 mega-rounds1, which accounted for US$2 billion of the total funding.

Most investors showed strong interest in late-stage2 FinTech firms which secured 10 out of 13 mega-rounds this year. This trend signals a shift in the strategy of investors across several ASEAN markets as they take a more cautious and risk-adverse approach of backing mature firms that are seen as standing a higher chance of emerging stronger from the pandemic. Given the growing adoption of digital payments in ASEAN, investors placed their confidence in, and injected the highest amount of funds into, late-stage FinTech firms from the payments sector.

Ms Janet Young, Head of Group Channels and Digitalisation, UOB, said, “The revival of investments in ASEAN’s FinTech industry has seen funding break through US$3.5 billion this year. Looking beyond this strong rebound, the opportunity to forge strong win-win-win partnerships between incumbent banks, FinTech firms and ecosystem platform players and expanding across the region will remain instrumental in propelling the sustainable growth of ASEAN’s FinTech firms.

“At UOB, we have long collaborated with FinTech partners to empower their growth with our deep understanding of the cultural, business and regulatory nuances in ASEAN and by connecting them to our regional ecosystem. Our close collaboration also enables us to tap on each other’s unique strengths and capabilities to create progressive financial solutions and seamless digital experiences that benefit our customers in an increasing online world.”

Vietnam takes third spot in FinTech funding, attracting two out of 13 mega-rounds

Vietnam-based FinTech firms saw a sharp rebound in funding, securing almost a tenth (nine per cent) of the total 167 deals, amounting to US$388 million in funding. The rebound in funding was attributed to two mega-rounds, namely US$250 million into VNPay, a mobile payment solutions provider for banks and businesses, and US$100 million into the series D fundraising round of MoMo, Vietnam’s largest e-wallet.

Singapore-based FinTech firms continued to attract the strongest funding in ASEAN, securing almost half (49 per cent) of the total deals, amounting to US$1.6 billion in funding. This includes six mega-rounds worth US$972 million in total. Indonesia retained its second position this year, raking in US$904 million in funding (26 per cent). FinTech firms in Singapore and Indonesia received funding in almost every category3, an indication of a vibrant and growing industry with an active investment scene.

Mr Shadab Taiyabi, President at SFA, said, “We are heartened that the FinTech scene across Southeast Asia continues to thrive and grow at a rapid pace, as attested by the strong rebound in financing this year. One key driver of this resurgence was the pandemic, which has catalysed digital adoption across the region, driving the rise in digital payments and accelerating the shift towards digital channels within the financial services sector.

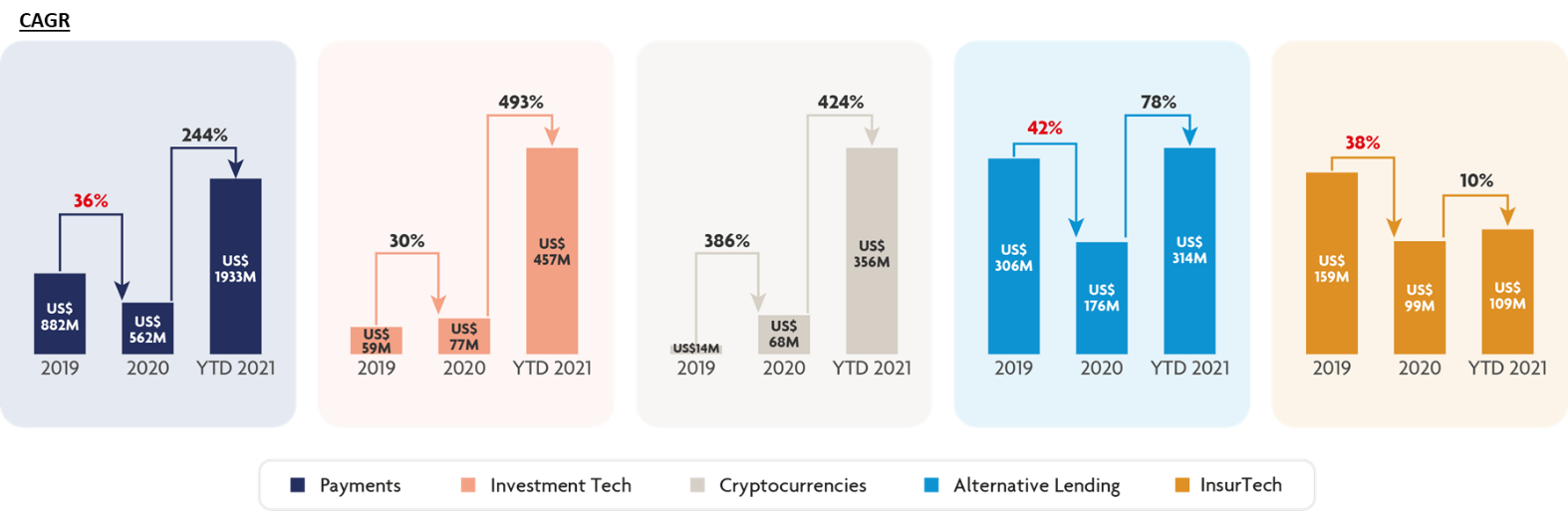

Funding in investment tech and cryptocurrency firms saw strongest growth

ASEAN FinTech funding trends by consumer related categories, 2019- YTD 20214

Funds injected to investment tech and cryptocurrency firms in ASEAN saw the strongest growth this year, taking both categories to the second and third place respectively after payments. This is also the first time in six years that alternative lending has been edged out of the top three spots in terms of funding given the increasing interest in digital investments and digital currencies among consumers.

Compared with 2020, funding for investment tech firms grew by six times to US$457 million this year, in line with growing consumer interest in the use of digital trading and wealth management tools. According to a survey5 conducted by UOB, PwC and SFA, six out of 10 ASEAN consumers have used digital tools such as robo-advisers and online brokerage platforms for their investment needs.

Funding for cryptocurrency firms came in third at US$356 million as they attracted five times the funding received in 2020. Given that nine in 10 ASEAN consumers have started or plan to use cryptocurrencies and central bank digital currencies6, the share of cryptocurrency firms in the region is expected to grow as players tap into consumers’ rising interest.

Payments remained the most funded FinTech category in ASEAN this year at US$1.9 billion and continued to make up the majority of FinTech firms in most countries, except for Singapore (cryptocurrency) and Thailand (alternative lending). Funding into these firms will accelerate the usage of e-wallets, debit and credit cards and mobile banking apps which are already the most popular payment methods among ASEAN consumers after cash7.

Ms Wanyi Wong, FinTech Leader, PwC Singapore, said, “Companies that have embraced FinTech are reshaping the marketplace. With digital payments becoming the norm, and areas such as wealthtech and crypto assets fast gaining interest, our research findings are indicative that consumers in ASEAN have come to embrace a wide range of FinTech solutions along with the digital experience, and that they are ready to take on the digital future. The question is no longer whether FinTech will transform the business landscape, but how to best adopt and embed a FinTech-centred strategy, underlined with inclusion, trust, transparency and accountability, to emerge as market leaders.”

References:

1Defined as a funding round of US$100 million and above.

2Late-stage FinTechs are defined here as Series C and above.

3The categories include alternative lending, banking tech, blockchain in financial services, cryptocurrencies, finance and accounting tech, insurance tech, investment tech and regulatory tech.

4First nine months of 2021.

5The survey was conducted in September 2021 among 3,086 respondents aged 18 to 55 and above, across Indonesia, Malaysia, the Philippines, Singapore, Thailand and Vietnam.

6Ibid.

7Ibid.